Subsidiaries of foreign groups: do not capitalize R&D expenses under French standards!

Abstract: To avoid any restatement under IFRS, subsidiaries of international groups may be tempted to capitalise R&D expenses under French standards. Not only does this approach offer virtually no advantages, but it also exposes them to unnecessary corporate income tax. Explanations.

Accounting principle of R&D expenses under IFRS.

Research outlays must be expensed, but…

Research must be expensed. IAS 38 prohibits the capitalisation of related expenses unless it can be demonstrated that there is an asset that will generate probable future economic benefits.

Capitalisation of development expenses is mandatory under certain conditions

On the other hand, project development expenses must be capitalised if the company can demonstrate that all recognition criteria (IAS 38 §57) are met, including: technical feasibility, intention and ability to complete, ability to use or sell, existence of probable future economic benefits, availability of resources, and reliable measurement of attributable costs.

… And according to the French GAAP (PCG)

Research costs are generally expensed….

The PCG accepts the capitalisation of research costs if they can be linked without interruption to a subsequent intangible asset (in this case, a development phase). Otherwise, they must be recorded as expenses. Article 212–3 of the PCG states:

“Expenses incurred during the research phase before the development phase must be recognised as expenses when incurred and cannot be included in the cost of an intangible asset at a later date.”

The PCG is therefore slightly less strict than IAS 38, which strictly prohibits capitalisation.

… And optional capitalisation of development expenses under certain conditions

Article 212–3 of the PCG (French GAAP) states:

“Development costs may be recognised as assets if they relate to clearly identified projects that have a reasonable prospect of technical success and commercial profitability.”

If an entity cannot distinguish between the research phase and the development phase of an internal project aimed at creating an intangible asset, it treats the expenses for that project as if they were incurred solely during the research phase.

The PCG sets the same capitalisation conditions as those laid down in IAS 38, in particular, the need to distinguish between the research phase and the development phase clearly.

And in practice

Activation of development costs to align with IAS 38:

Points to note

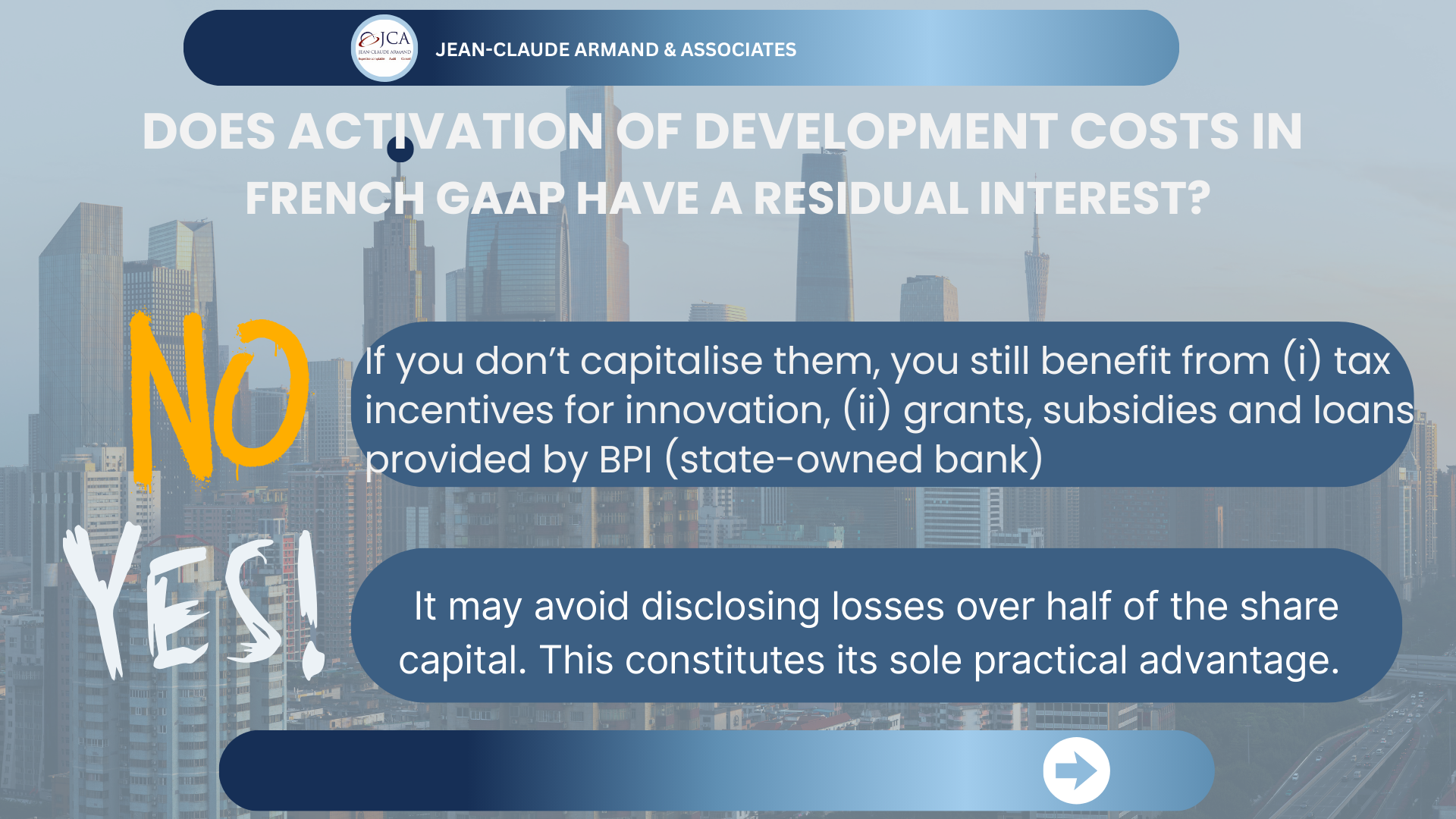

To avoid any restatement under IFRS, subsidiaries of foreign groups may be tempted to capitalise development costs under French GAAP.

However, in doing so, they must take two precautions. First, they must ensure (i) that the conditions used to capitalise these costs under French GAAP are also those under IAS 38 (which is more restrictive than PCG) and (ii) that this capitalisation does not lead to unnecessary corporate income tax payments.

Very limited residual interest in capitalising R&D expenses

The BPI (the French state-owned bank responsible for assessing subsidies and aid) and banks now deduct the net book value of R&D expenses from equity, which is one of the criteria for determining subsidies.

Furthermore, capitalising R&D expenses has no impact on eligibility for innovation tax incentives (research tax credit (CIR) and/or young innovative company (JEI) status). In other words, subsidiaries of foreign groups can benefit from these incentives without capitalising development expenses.

However, capitalising development costs prevents the startup from disclosing equity capital of less than half of its share capital. The latter is, in fact, its only interest.

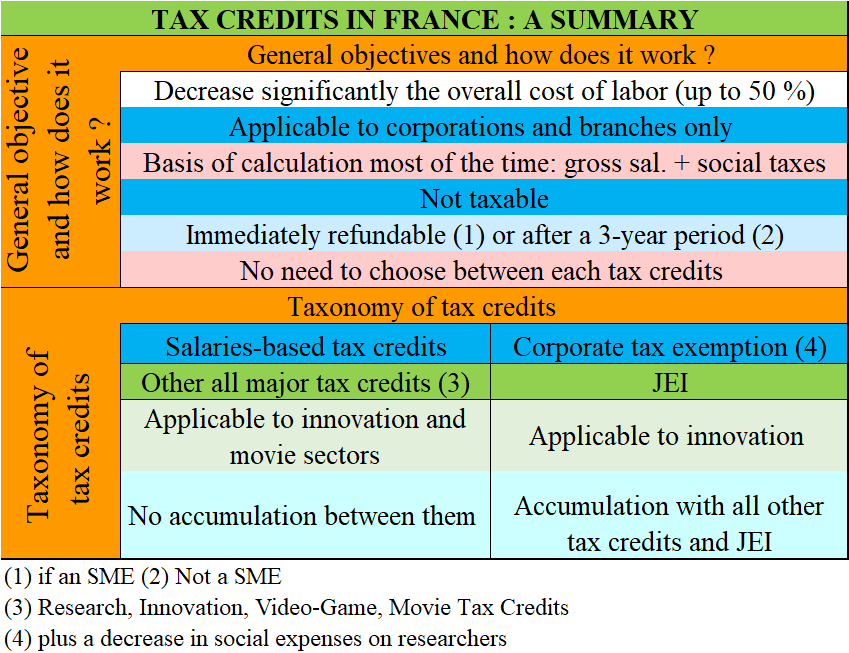

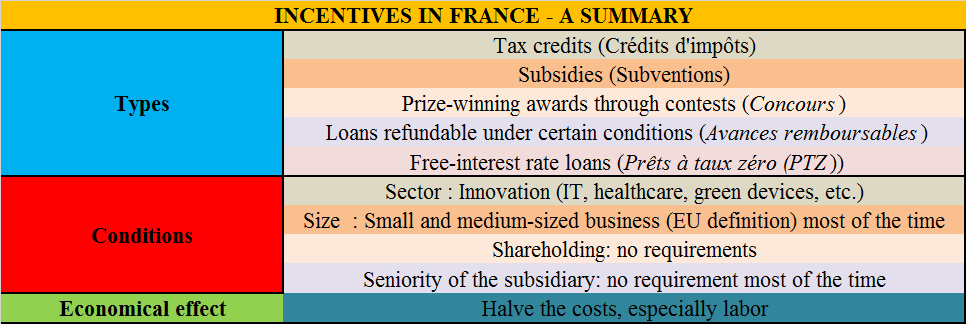

To sum up, how to process R&D expenses

: how to take advantage of it? Summary")