Reduced taxation on software (IP BOX): how can you benefit?

Reduced taxation on software (IP BOX) – Abstract

After having detailed the basic conditions in the article IP BOX – how can you benefit, we now turn to the application conditions for benefiting from the reduced rate of taxation on software, a complex scheme that is little-known to software publishers, especially subsidiaries of Foreign companies and startups.

About the conditions of application

Formal requirements

The decision to opt for this system must be made at the latest when filing the tax return and is evidenced by the completion of appendix no. 2468-SD (CERFA no. 16008). A company that ceases to file this declaration permanently loses the benefit of the option not only for the year in question but also for subsequent years.

The option applies to all concession products. In other words, the company waives the right to place them totally under the ordinary law regime.

Lastly, per article 13 BA of the General Tax Code (CGI), the company must provide documentation justifying the calculation method chosen by the company for each asset or group of assets: this includes in particular

- The organization of the company’s research and development activities, as well as the process for determining taxable income for assets transferred or licenses granted (see substantive conditions below),

- A full description of the intangible assets concerned, a discussion of the application of a reduced tax rate and the method of allocating costs to each asset (see substantive conditions below),

Documentation must be (i) accessible in a compatible electronic format to facilitate exchange and reading by the administration, excluding “PDF image” formats from scans, (ii) written in French or translated if necessary, (iii) contain verifiable electronic data for calculations and analyses.

Background requirements

As the spirit of the system is to ensure traceability between the asset and the associated source of revenue, the option cannot be global but only per software or group of software, following organizational and commercial logic (coherence between research activity and segmentation of the commercial offer).

The methodology for segmenting taxable income at the reduced rate must remain consistent from one year to the next. In short, there must be permanence in the methods used to determine taxable income at a reduced rate over time.

Reduced taxation on software: detailed calculation

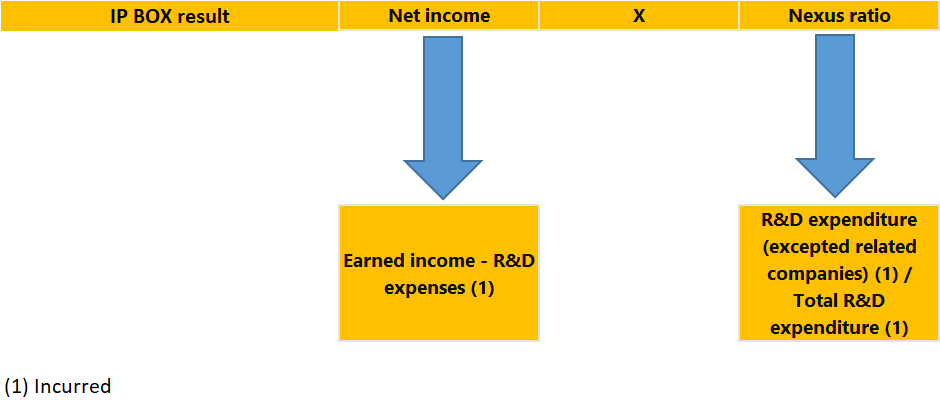

The 2 aggregates used in the calculation are net income and the Nexus ratio.

Income and expenses included in net income

It is determined as follows:

- Income from disposals or concessions relating to the asset concerned,

- R&D expenditure incurred indirectly by the company in connection with the creation of the asset.

Broadly speaking, they correspond to direct R&D expenditure. Unlike the Research Tax Credit, indirect expenditure is excluded, notably

- Operating costs, regardless of whether they are determined on an actual or flat-rate basis,

- Expenditure to protect industrial property rights,

- Technology watch expenses incurred during R&D operations.

The CIR does not reduce R&D expenditure.

The expenses to be taken into account are all those incurred as from the exercise of the option. Expenses incurred before the year in which the option is exercised cannot be taken into account.

The Nexus ratio

The result as determined above is multiplied by a Nexus ratio, which aims to neutralize R&D expenses invoiced by companies or branches linked to the entity benefiting from the IP Box, in order to retain only those invoiced under arm’s length conditions. As an exception, expenses rebilled without margin by affiliated companies can be retained.

In a nutshell,

- in the numerator, R&D expenditure excluding affiliated companies,

- in the denominator, R&D expenditure excluding affiliated companies,

The ratio is calculated on a cumulative basis from the origin of IP Box expenditure.

Schematically, the income required to benefit from reduced taxation on software (IP Box) is determined as follows:

Reduced taxation on software

Reduced taxation on software: example

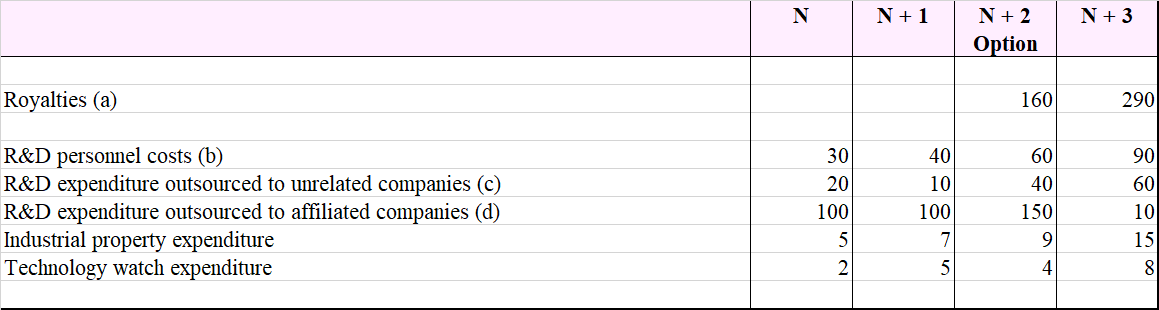

A software company based in France begins an R&D program in fiscal year N. In fiscal year N+2, this program leads to the receipt of royalties. During fiscal year N + 2, this program leads to the collection of royalties in N + 2, enabling the publisher to opt for the tax treatment provided for the reduced taxation on software. The first revenues generated by patent X are recognized in fiscal year N + 3: R&D expenditure and royalties are as follows:

The data

Reduced taxation on software

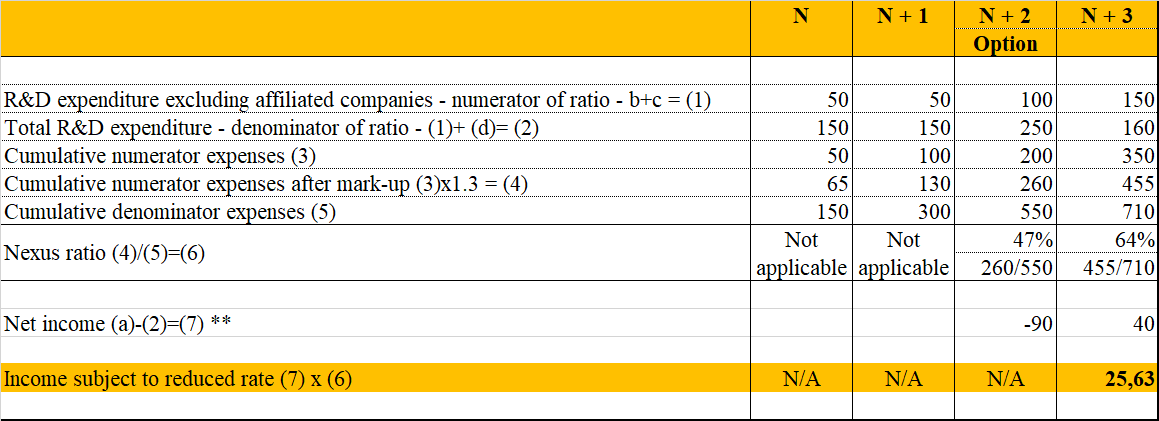

And the solution

Reduced taxation on software