Letting furnished property in France: what you need to know

Letting furnished property in France: abstract

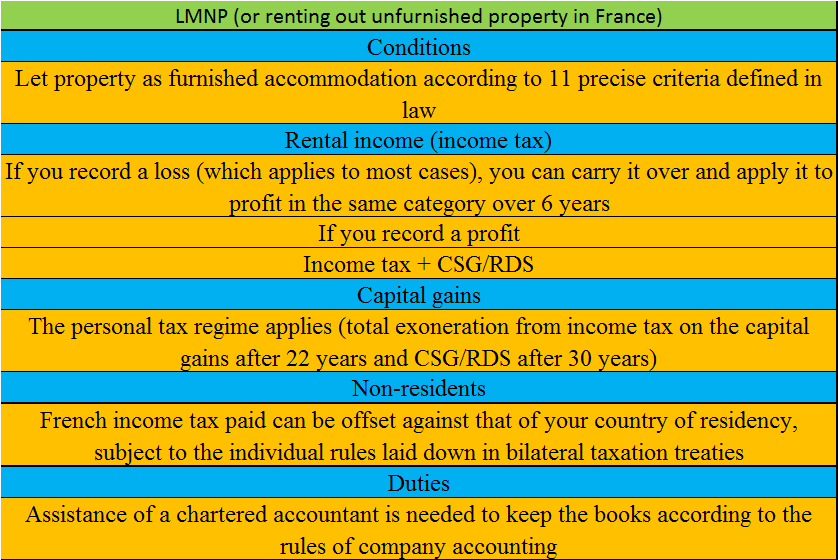

Have you ever considered letting furnished your property (Loueur Meublé Non Professionnel)) in France? Because the LMNP is a tax niche that allows you to benefit from (i) the advantages of company taxation on the rental income and (ii) the advantages of personal taxation on the capital gains. If you think this solution is for you, you also need the assistance of a chartered accountant. Let us explain.

Letting furnished property in France and income from property rentals.

Rather than let your property in the usual French way (unfurnished), rent it out furnished. The apartment should meet 11 criteria by law and be rented out to a person who uses it as a principal residence. This will allow you to deduct all the costs you incur as a landlord. In practical terms, it means that you can deduct from the taxable income (i) the depreciation of the property (ii) all the purchase costs (stamp duty, conveyancing fees) and (iii) the day-to-day costs of owning a property (management company charges, insurance, costs of repairs, etc.), local taxes and interest payments.

If you rent out your property unfurnished, you cannot depreciate the property, nor can you deduct the purchase costs or some of the running costs (those of a caretaker in particular).

Also, given the rules for calculating the taxable income, which are far more favourable for furnished rentals than unfurnished ones, you will probably record a loss in the first case, but a profit in the second.

To use this arrangement, you must use company accounting, which by law requires a chartered accountant.

Renting out furnished property and capital gains

Letting furnished property and gains – the rules in detail

Even though you can deduct the depreciation of rental properties from your taxable income, the accumulated depreciation is never subtracted from the gross value to calculate capital gains. In other words, the rules of company accounting do not apply. Rather, the capital gains tax is calculated according to the rules for personal taxation. You benefit from a sliding scale of taxation on the price of sale throughout the time you own the property, so that you are totally exonerated from income tax on the capital gains after 22 years, and from the CSG/RDS social security charges (if these apply to you) after 30 years.

Letting unfurnished property and gains – a summary

To sum up, capital gains on property calculated according to personal taxation rules by and large taxed less than those computed according to company taxation.

Letting furnished property for French tax residents…

If you are fiscally resident in France, losses from letting a property as LMNP are not deductible from your overall income because they do not come from a professional activity. They can, however, be applied to income of the same type over the following 6 years (10 years before 1 January 2017). If you have recorded a profit, it is added to your overall income and taxed as income according to your tax band (IRPP – impôt sur le revenu des personnes physiques). In addition to this, you will pay the social security charges CGS/RDS (15.50% of the taxable income).

As for the capital gains, they are taxed as income in the same way as the rental income.

…And for non-residents

If you are not a French tax resident, you must submit a tax return to the centre for non-residents. As long as a property is situated in France, it is taxable in France. When your taxable income only concerns the LMNP, this tax return becomes a simple formality.

Taxes on capital gains from property are levied at the proportional rate of 34.5% and paid on the day of sale.

If, however, you pay income tax and CSG/CRDS, you can deduct this from the tax paid in the country in which you are resident, subject to the double taxation avoidance treaty that may exist between your country and France.

Renting out furnished property in France, a summary

Jean-Claude ARMAND and Partners assist you in benefiting from this tax niche.