Liaison office branch or subsidiary: how to choose?

Liaison office branch or subsidiary : In other words, in order to establish a business in France, does a foreign company have to systematically create a subsidiary company? In other words, can we find solutions more flexible, less expensive? A simple registration towards social bodies to hire staff, or a liaison office, or a branch. The answer to this question depends not only on the means that will be deployed in France.

In which circumstances consider a liaison office in France or a branch with no activity …

When the foreign company simply wishes to hire one staff aimed at having contacts, collecting information, giving information for the mother company’s account, or assuming the advertising of it. In other words, its employees are never allowed to sign any order forms. This task is performed by the mother company’s representatives in the country of origin. To decide which the most suitable option is between a simple SIRET number and a liaison office, – click here.

Concerning fiscal law, the liaison office does not have a literal existence. The charges of the liaison office are in principle deductible from the taxable income of the foreign company in its country of origin. However, if the liaison office has in fact commercial activities, it can be requalified as a permanent establishment (see below).

…Or a branch with activity or a subsidiary

If the activity within France is commercial, the mother company has to create a branch with activity.

According to the French tax regulations, such a branch is considered as a permanent establishment, which designates for the purpose of tax treaties between countries of the OECD, a fixed establishment of business where the company practices all or a part of its activity: Are in particular permanent establishments, headquarters, transformation plants, construction sites which in time exceed 12 months. Are not considered as permanent establishments, non-commercial activities as storage, exposition, delivery, transformation by another company, etc.

Consequently, the branch is subject to corporate tax according to the common law rate. To determine its fiscal income (for both corporate tax and VAT purposes), the accounting income needs to be restated, as if the branch were a separate legal entity.

Finally, the company can create a subsidiary company; which is detached from the mother company. The income is taxed in France (see Milestones when starting a business in France)Milestones when starting a business in France.

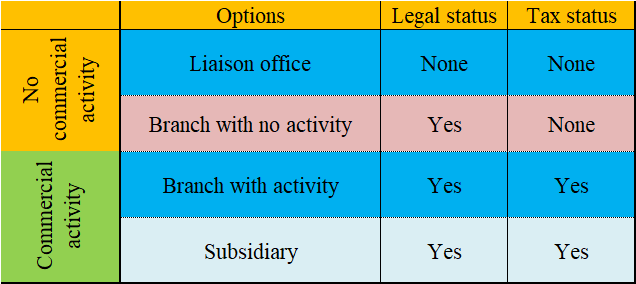

The aforementioned writings may be summarized as follows:

Liaison office branch subsidiary

Jean-Claude Armand and Partners advices you to choose the establishment structure in France (liaison office, stable establishment, subsidiary company).

Need more information?