Tax in France

Overview

When it comes to talking about tax in France, keep the following in mind: more than in any other country, the more important a company is the greater the burden of taxes and duties it must bear in relation to turnover.

Corporation Tax in France

Individual entrepreneurs whose business is not considered a trade activity declare their results based on their cashbox accounts.

All other businesses, particularly corporations, draw up their taxable income in two stages: first of all, they determine their results according to the rules of the [French] General Chart of Accounts. In other words, the book result determined for tax purposes is exactly the same as that mentioned in the financial statements (see accounting regulations). Next, a certain number of charges or products are added or deducted to arrive at the taxable income. Among the deductions are equity interests which benefit, under certain conditions, from an 88 or 95 % reduction off the amount booked, depending on whether they relate to dividends or assignments of shares.

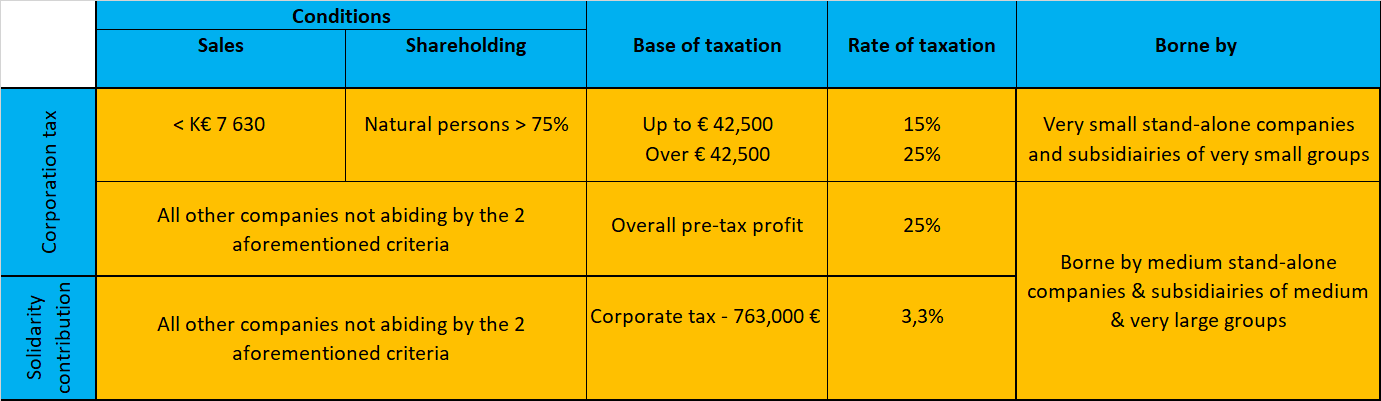

This taxable income is subject to a rate of 25% (the standard rate). The rate is however decreased to 15% – up to €42,500 – if the company meets the two following conditions: natural persons own over 75% of company or of the the parent company: (ii) its sales are lower than K€ 7,630.

The corporation tax burden is submitted to an additional 3.3% contribution if one of two above conditions (natural shareholding persons >75%, turnover < K€ 7,630) are not met. The figure as calculated before is subject to a € 763,000 deductible.

The rows as outlined above can be summarized as follows:

Corporation tax in France

Refunds/deductions are not meant to significantly alter the effective tax rate (corporation tax/pre-tax profit) unless the deductions are applied to tax credits. Under certain conditions, any company can have between 30% of its research & expenses refunded through the CIR. They can benefit from the statut JEI- Young Innovative Company Status under certain conditions as well.

Withholding at source

Dividends sent by French affiliates to their shareholders located in USA and the UK have a 5% withholding rate applied, since they hold at least 10%. Amounts paid to corporations located in the United States undergo a 5% withholding at source, and sums paid to British companies have no withholding applied.

Value Added Tax in France (VAT)

All commercial transactions, except in a few rare occasions, are subject to value added tax (VAT), except those benefiting companies that are not-domiciled in France. In principle, the VAT paid on acquisitions is not a charge for the company because it can be deducted from the VAT billed and collected from sales.

There are two VAT rates. The normal rate, 20%, applies to all transactions, goods and services. As an exception, transactions involving consumer staples (foods, pharmaceutical products, culture) undergo a tax rate of 5.50%.

Since the VAT is borne by the customer in the end, the tax debtor according to law is always the company billing and not the customer. The company must file a VAT statement, more often than not on a monthly basis, or quarterly in the case of small enterprises or individual entrepreneurs.

Personal Income withholding tax (Prélèvement à la source)

Although employees’ income tax is withheld from their pay stubs, the tax debtor according to law is the company, not the employees. Companies file a return and pay it on a monthly basis when triggering payment of other social taxes.

Local taxes

From 01/01/2023 onwards, to beep up France’s competitiveness, the main local taxes, the Territorial Economic Contribution (CET) and the Economic Added Value Contribution (CVAE) were suppressed.

Need more information?